Service Design Case Study: NatWest Better-off Programme

Project Background

Setting the Stage: The Ambition of the Better-off Programme

NatWest faced a pivotal opportunity: to transform how it supported customers in managing their savings, moving beyond a simple ‘set-and-forget’ mentality towards a dynamic, intuitive partnership that adapted to the ebb and flow of their lives. Our mission was to deepen this engagement, empowering customers to not just save, but to achieve their financial aspirations with NatWest as a proactive guide.

The initiative, formally known as the Better-off Programme, was born from this ambition. We set out to empower customers in establishing and actively managing their diverse, often competing, personal savings goals. A critical first step was to streamline the existing savings journeys, making them far more intuitive. This simplification wasn’t just about ease of use; it was strategically designed to significantly boost user engagement and fundamentally shift customers away from a passive approach to managing their financial futures. Our collective aim was to refine these journeys into a robust minimum viable product (MVP), ready for a focused pilot programme. This also meant fully developing any journey segments that were not yet complete and rigorously testing all new UX/UI designs to ensure a seamless and effective user experience.

Our primary focus crystallised around three core areas, or ‘key epics,’ that would define the new service: first, equipping customers to clearly and effectively set their savings goals; second, actively supporting them in maintaining progress towards these goals; and third, providing clear, accessible pathways to accelerate their savings. The foundational qualitative research that breathed life into these epics involved 39 hours of detailed one-to-one interviews, meticulously conducted with customers across London and Edinburgh over an intensive eight-week period. This deep dive into their financial lives and aspirations was paramount to shaping a service that would truly resonate.

Understanding the Hurdles: Customer Realities and Strategic Questions

As we delved deeper, two primary, interconnected service design challenges came into sharp focus. For the customers we aimed to serve, the fundamental question was: how could we genuinely simplify the often daunting process of initiating and, crucially, achieving their savings goals? We needed to position NatWest not just as a bank, but as an actively helpful and enabling guide throughout their unique financial journeys. Simultaneously, from NatWest’s perspective, a strategic question loomed: how could the bank organically and effectively introduce its lending products to customers who were primarily focused on saving, without appearing opportunistic or disrupting their existing financial goals?

Our research quickly illuminated the everyday realities that make consistent saving so difficult. We deeply understood that unexpected life events and the natural fluctuations of financial circumstances can easily disrupt even the most carefully laid plans. Many individuals, we found, tend to save for a generalised ‘rainy day’ rather than for specific, clearly articulated objectives. This often meant that savings lacked a strong motivational anchor. Furthermore, their perception of borrowing was typically one of caution, viewing it as a last resort in their financial toolkit rather than a proactive option for achieving larger goals. These human elements were central to the challenges we needed to address.

Crafting the Path Forward: Strategy, Principles, and Design Philosophy

With a clear view of the hurdles, our overarching strategy began to take shape, centering on meticulously refining the three key epics that would define the customer’s enhanced savings journey. For Goal Setting, we envisioned a straightforward and empowering experience, enabling customers to clearly articulate, express, and frame their unique financial aspirations. When it came to Goal Maintenance & Saving, our focus shifted to helping customers easily visualise their progress, feel genuinely supported as they saved, and receive contextual, timely suggestions for effective savings tactics. Finally, the Accelerate epic was about thoughtfully offering customers a curated range of relevant tips, practical tactics, and appropriate financial products, all designed to help them reach their goals more quickly and efficiently.

This strategic framework was not built in a vacuum; it was underpinned by a series of guiding principles and a deeply considered design philosophy. We rigorously tested several key product hypotheses that we believed were critical to success. These included the importance of building ‘Momentum for Saving,’ fostering a sense of ongoing progress; establishing a flexible ‘Better Off Eco System’ of interconnected and mutually supportive services; encouraging positive ‘Habit Forming’ behaviours around saving; maintaining a ‘Continuous Presence’ throughout the customer’s financial journey, offering support at the right moments; utilising ‘Recognisable Patterns’ in our designs for intuitive interaction; and enabling clear ‘Goal Expression’ to allow for truly personalised experiences.

Our design thinking was further sharpened by a set of core Experience Design Principles that served as our compass. We committed to concepts like ‘Join the dots for me,’ which meant translating complex financial insights into meaningful and actionable steps for the customer. ‘Default in my favour’ guided us to implement proactive defaults that would genuinely benefit the user. We embraced ‘Ladder up,’ a principle focused on starting with small, achievable steps to build customer confidence and motivation. Our commitment to ‘Life over numbers’ pushed us to reframe finance in terms of tangible life goals rather than abstract figures. The principle of being ‘On your side’ ensured we offered supportive suggestions, not perceived judgements. Through ‘Hold my hand,’ we aimed to build trust and clarity with transparent guidance. ‘One size fits one’ reminded us to tailor interactions to individual needs as much as possible. And finally, ‘Lighten up’ encouraged us to engage users with thoughtful, perhaps even playful, rewards and acknowledgements to maintain their motivation along the way.

Beyond these foundational principles, we also adhered to several core thematic considerations that wove through our design process. We envisioned creating a flexible ‘product ladder,’ allowing for seamless entry into the savings ecosystem regardless of a customer’s starting point. We knew we had to cater for diverse goal types, with a specific focus on medium to long-term aspirations, while also identifying those goals that might naturally align with lending products. A critical element was ensuring customers prioritised the establishment of an emergency fund as a safety net. We also gave careful thought to how we could thoughtfully integrate lending products within the broader savings journey, making them feel like a natural extension of support. And consistently, we emphasized using simple, universally understandable language and finding moments to celebrate small successes to maintain ongoing motivation and a positive relationship with saving. These layers of strategy, principles, and thematic considerations collectively formed the bedrock of our approach to redesigning the NatWest savings experience.

Experience Design Principles: Guiding Our Approach

Our design approach was anchored by four core Experience Design Principles that emerged directly from our customer research findings. These principles served as our compass throughout the project, ensuring every design decision addressed real user needs:

1. “Join the dots for me”

The Principle: Translate complex financial data into meaningful, actionable recommendations that reduce cognitive load.

How We Applied It: Rather than overwhelming customers with raw financial data, we created context-aware recommendations that automatically connected their life circumstances to relevant savings opportunities. The system would surface the right suggestion at the right time, helping customers see the path forward without having to analyse complex information themselves.

Research Insight: Our interviews revealed that customers felt paralysed by financial complexity. They wanted guidance, not just data.

2. “Default in my favour”

The Principle: Implement sensible defaults and automated options that work in the customer’s best interest, using opt-out rather than opt-in patterns.

How We Applied It: We designed the service to automatically suggest sensible savings amounts based on spending patterns, pre-select protective options like emergency fund prioritisation, and enable frictionless automated payments. Customers could adjust these defaults, but we ensured the starting point was already optimised for their benefit.

Research Insight: Customers signalled strong commitment when they set up automated payments (Standing Orders), viewing this as a sign of serious intent.

3. “Ladder up”

The Principle: Use progressive disclosure to provide simple entry points while making depth available for those who want it, scaffolding learning along the way.

How We Applied It: We created a product ladder that allowed customers to enter the savings ecosystem at any level—whether starting with a simple rainy day fund or managing multiple complex goals. The interface revealed complexity gradually, building confidence through small wins before introducing more sophisticated features.

Research Insight: Smaller, achievable goals provided customers with quick psychological wins, while larger goals felt distant and overwhelming.

4. “Life over numbers”

The Principle: Frame financial goals in terms of life aspirations rather than abstract numbers, emphasising flexibility for unexpected life events and creating emotional connection.

How We Applied It: Instead of asking “How much do you want to save?”, we asked “What do you want to achieve?” The goal-setting experience centred on life events—holidays, home improvements, education—with the financial mechanics supporting these aspirations rather than dominating the conversation. Crucially, we built in flexibility for when “life happens,” allowing customers to adjust goals without feeling like they’d failed.

Research Insight: The most consistent theme from our research was that unexpected expenses derail savings plans. Customers needed permission and tools to adapt their goals to life’s realities.

Uncovering Insights: Our Research and Engagement Process

To truly understand the nuances of customer behaviour and build a service that resonated, we employed a robust mixed-method research approach. Our journey into the hearts and minds of NatWest’s customers began with a broad quantitative survey in ‘Sprint Zero,’ gathering responses from 500 participants. This provided a wide-angle lens on savings habits and attitudes. We then sharpened our focus with a mixed qualitative and quantitative survey, where over 30 participants completed a 15-minute online questionnaire using Usability Hub, offering targeted feedback on specific concepts. However, the richest, most layered insights emerged from an intensive eight-week period of in-depth, one-to-one qualitative interviews. We spent 39 hours in conversation with customers in London and Edinburgh, listening to their stories, understanding their challenges, and capturing their aspirations. A significant part of our subsequent analysis involved meticulously mapping the key behavioural insights gleaned from this deep qualitative dive to understand their direct design implications for the NatWest Better-off programme.

Our stakeholder engagement strategy was thoughtfully targeted, primarily focusing on distinct customer segments we had identified as crucial to the program’s success. The ‘Aspiring Starters’ and ‘Reactive Pragmatists’ were our primary target audiences for service design interventions, with the ‘Ambitious Climbers’ forming a vital secondary audience. While the presentation materials we drew from didn’t extensively detail every interaction with other internal bank stakeholders, their collaborative involvement was understood to be integral to the holistic success of the project and the eventual service implementation.

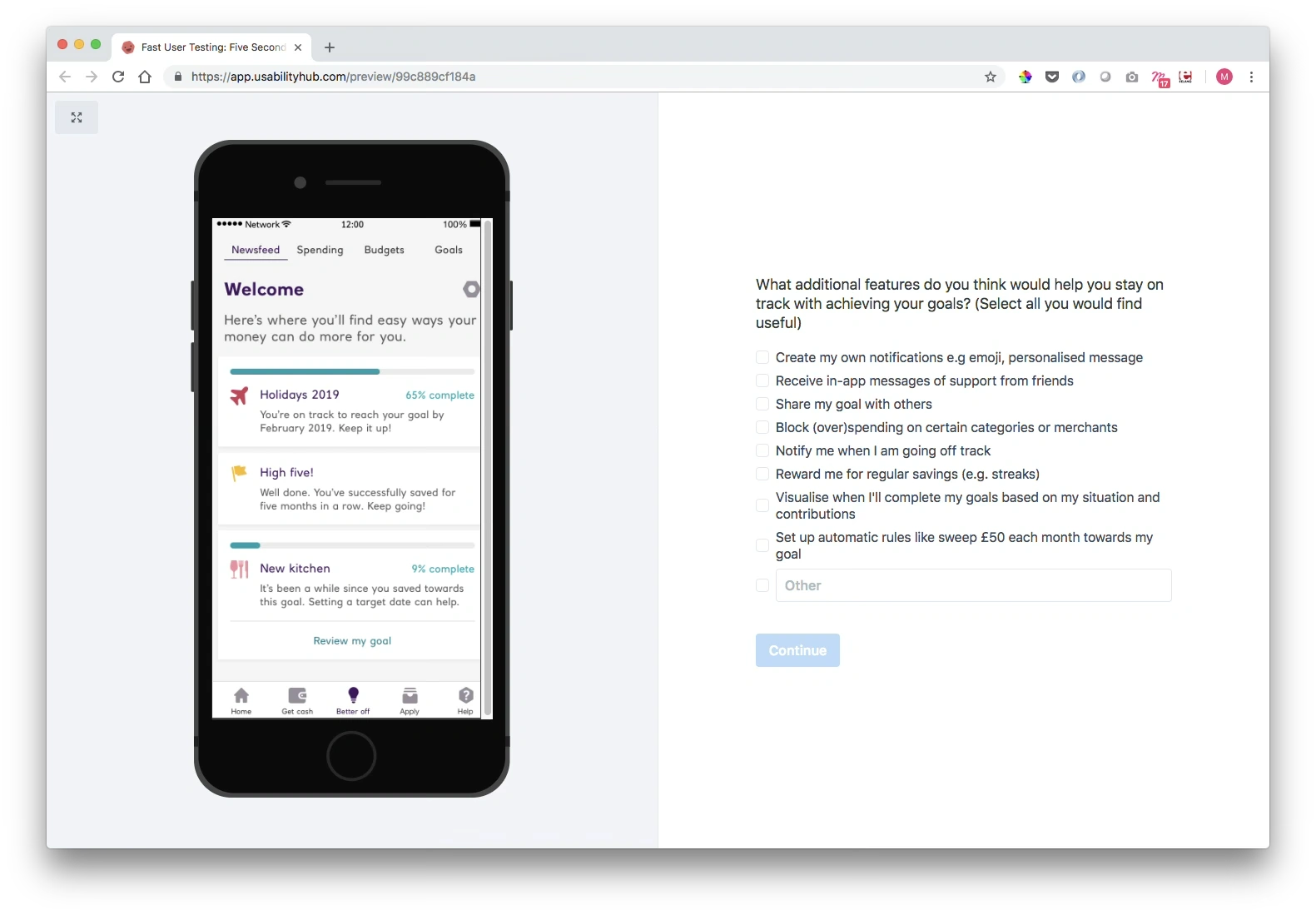

With a wealth of research insights in hand, we moved into development and validation. We meticulously crafted the UX/UI designs for the updated service journeys, ensuring they embodied the needs and desires uncovered in our research. These designs weren’t left to chance; they were rigorously tested using a combination of agile methods. In-house and in-branch ‘guerrilla’ testing allowed for rapid feedback, while remote testing sessions, facilitated by UsabilityHub, provided broader reach and diverse perspectives. The specific software tools utilised for the UX/UI development, though not detailed in our source presentation materials, supported this iterative process of design, test, and refine.

Behavioral Insights Discovered

Our research uncovered critical insights about customer psychology and behavior patterns that fundamentally shaped our design decisions. These findings challenged conventional assumptions about savings behavior and revealed the human realities behind financial decision-making:

Insight 1: “Life Happens” — Unexpected Events Derail Plans

What We Discovered: Emergency expenses consistently derail even well-intentioned savings plans. Customers expressed deep self-criticism about their saving habits, and temporarily “dipping into” savings was a common, often necessary occurrence rather than a failure.

Design Implication: We built flexibility into the core of the experience. Rather than treating goal adjustments as failures, we designed the system to accommodate life’s realities—allowing customers to pause goals, adjust targets, and redirect funds without guilt or friction. The interface normalized these adjustments as part of responsible financial management.

Why This Matters: Traditional savings products penalize flexibility. By embracing the reality that “life happens,” we positioned NatWest as understanding and supportive rather than judgmental.

Insight 2: Most Save Without Specific Objectives

What We Discovered: The majority of customers saved because it felt like “a good thing to do” rather than for specific goals. Savings were typically directed toward vague “rainy day” funds, and most people maintained only a few, often quite abstract, savings goals.

Design Implication: We couldn’t force goal specificity onto customers who didn’t naturally think that way. Instead, we created a spectrum of goal types—from explicit, defined objectives (holiday, house deposit) to more open-ended “safety net” goals. The system respected both approaches equally, providing structure where customers wanted it while supporting more fluid saving patterns.

Why This Matters: Forcing all customers into rigid goal-setting would have created friction and abandonment. Acknowledging diverse saving styles increased accessibility.

Insight 3: Automated Payments Signal Strong Commitment

What We Discovered: When customers set up Standing Orders or automated transfers, they viewed this as a powerful signal of their own commitment to a goal. The act of automating wasn’t just convenient—it was psychologically meaningful.

Design Implication: We made automated payment setup a celebrated moment in the goal creation flow. The interface emphasized that automating payments demonstrated commitment and increased success probability. We also surfaced progress on automated goals more prominently, reinforcing the positive association.

Why This Matters: By recognizing and amplifying the psychological power of automation, we could encourage behavior change that genuinely helped customers succeed.

Insight 4: Flexibility and Control Are Paramount

What We Discovered: Customers universally valued transparency in terms and conditions and deeply desired the intrinsic ability to flexibly adjust their goal parameters. They wanted their savings plans to adapt to their evolving life circumstances rather than feeling rigidly locked in.

Design Implication: We designed for maximum user control at every stage. Goal parameters could be adjusted at any time, contributions could be paused or modified, and funds could be reallocated between goals. All terms were presented in plain language, and the consequences of any action were clearly previewed before confirmation.

Why This Matters: When customers feel trapped or controlled, they disengage. By prioritizing autonomy and transparency, we built trust and long-term engagement.

The Unfolding Picture: Findings, Learnings, and Future Impact

While specific quantifiable metrics from a pilot programme or other direct quantitative results were not explicitly detailed in the initial information shared with us, our comprehensive design process successfully delivered a set of meticulously refined customer journeys and thoroughly validated UX/UI designs. These were primed and ready for further development and eventual rollout.

Drawing from our profound understanding of customer behaviour and their articulated needs, we formulated several actionable recommendations to guide the programme’s evolution. For instance, we strongly advised implementing the flexibility for users to easily adjust their goal parameters as their circumstances changed. We also highlighted the importance of actively encouraging customers who did not yet have savings accounts to seamlessly open one, integrating this into the journey. Furthermore, we emphasized that any ‘accelerate’ options presented to customers should include a comprehensive and balanced mix of practical tips, effective savings tactics, and relevant, clearly explained financing products.

Our research journey provided significant, nuanced learnings about customer behaviour and their intricate relationship with savings. These insights became the bedrock of our design decisions:

- ‘Life Happens’: A consistent theme was the impact of the unexpected. Emergency expenses often derail savings plans, people can be remarkably self-critical about their saving habits (or perceived lack thereof), and temporarily ‘dipping into’ savings is a common, often necessary, occurrence.

- ‘Saving Habits’: We observed that many individuals save because they instinctively feel it’s a generally ‘good thing to do,’ frequently without a specific ‘why’ or primarily for a vague ‘rainy day’ fund. Most people tend to maintain only a few, often quite abstract, savings goals. Interestingly, regular, automated payments like Standing Orders are perceived as a strong sign of personal commitment to a goal.

- ‘Goal Perceptions’: The way customers perceive their goals also varied considerably. Medium to long-term goals frequently feel distant and less pressing than immediate financial needs. Conversely, smaller goals often serve a more temporary, ‘lightening’ purpose, fulfilling short-term desires or providing a sense of quick accomplishment.

- ‘Attitude to Borrowing’: We unequivocally confirmed that customers generally possess a cautious ‘Attitude to Borrowing.’ It’s typically viewed as a last resort, although this stance softens for significant, pre-defined life events like a house deposit or in truly unexpected emergency situations.

- ‘Feeling of Being in Control’: This emerged as paramount for customers. They profoundly value transparency in terms and conditions and universally desire the intrinsic ability to flexibly adjust their goal parameters, allowing their savings plans to adapt to their evolving life circumstances rather than feeling rigidly locked in.

A Concluding Vision for NatWest’s Better-off Programme:

Ultimately, our service design work for the ‘Better-off programme’ laid out a clear and actionable roadmap to genuinely support NatWest customers in successfully managing their savings with greater autonomy, confidence, and a true sense of partnership. By anchoring our approach in a deep understanding of genuine user needs, leveraging rich behavioural insights, and proposing a meticulously refined MVP built around the key epics of goal setting, maintenance, and acceleration, we aimed to create a definitive “win-win.” This envisioned a savings experience that would not only empower customers to achieve their diverse financial aims but also position NatWest as an exceptionally trusted, enabling, and proactive partner. The journey was about reimagining financial well-being, helping customers to not just save, but to thrive.